We take your security very seriously. In order to protect you and our systems, we are making changes to all HSBC websites that means some of the oldest web browser versions will no longer be able to access these sites. Generally, the latest versions of a browser (like Edge, Chrome, Safari, etc.) and an operating system family (like Microsoft Windows, MacOS) have the most up-to-date security features.

If you are seeing this message, we have detected that you are using an older, unsupported browser.

In 2022 global investors are faced with a new set of challenges including slower growth, monetary policy tightening and lower asset returns even as the pandemic persists amidst the emergence of new Covid variants and geopolitical risks are heightened. Against this backdrop, Asian markets offer pockets of investment opportunities, supported by faster economic growth when compared with developed markets and attractive earnings and valuation profiles. Asian equities, in particular, stand out in this environment after being unloved in 2021.

In the coming years we see Asia leading global growth and cementing its position as a greener and more technologically advanced economic powerhouse amidst demographic shifts, policy reforms and rising innovation. However, Asian assets continue to be underrepresented in global portfolios, a situation that is ripe for change. At HSBC Asset Management, we have been helping our clients navigate various market cycles and connecting them, for decades, to underexplored opportunities in the region – catalysing the inevitable transition to Asia.

Focus on Asian equities

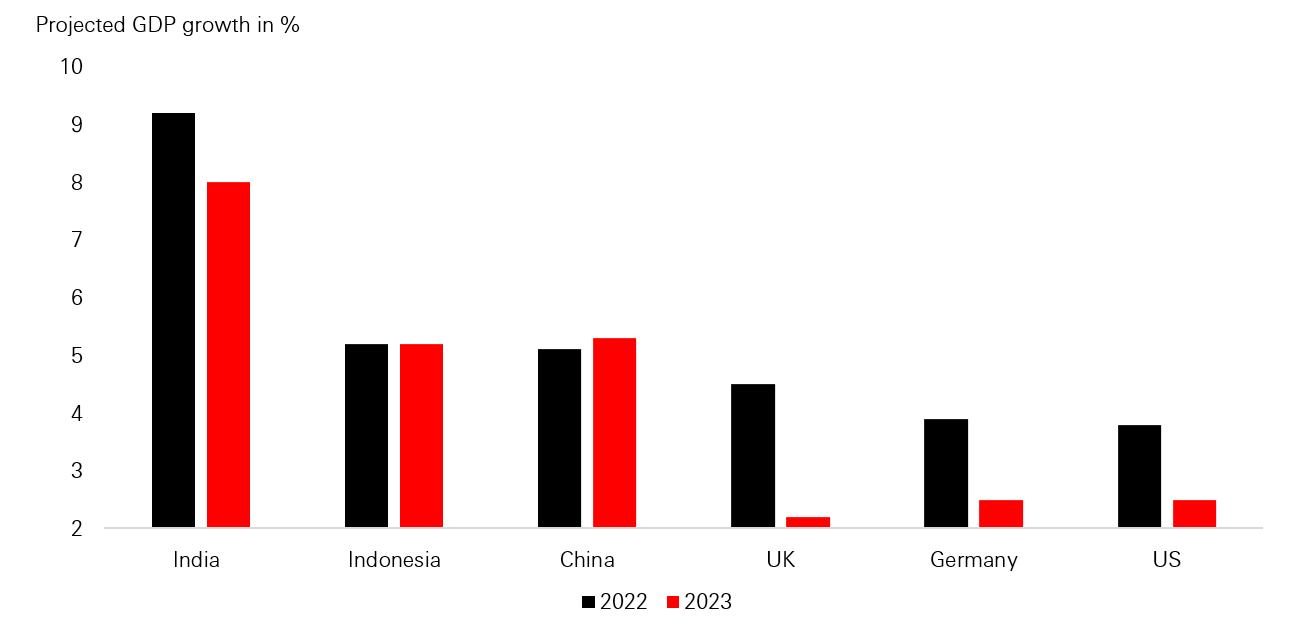

Asian economies continue to strengthen

We see Asia’s growth recovery strengthening in 2022, enabling a virtuous and sustainable economic cycle in the region

In contrast to the tightening cycles in developed markets, China is on the easing path and its policy tilt is expected to be the key driver of the regional recovery

Finally, Asia’s stronger footing, underpinned by its exports, capex and productivity growth, can help the region weather exogenous shocks

Asian economies gain strength on exports, capex & productivity

The performance figures displayed in the above relate to the past and past performance should not be seen as an indication of future returns.

Source: Refinitiv, HSBC Asset Management, January 2022. For India, the year runs from 1 April to 31 March the following year.

Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative purpose only.

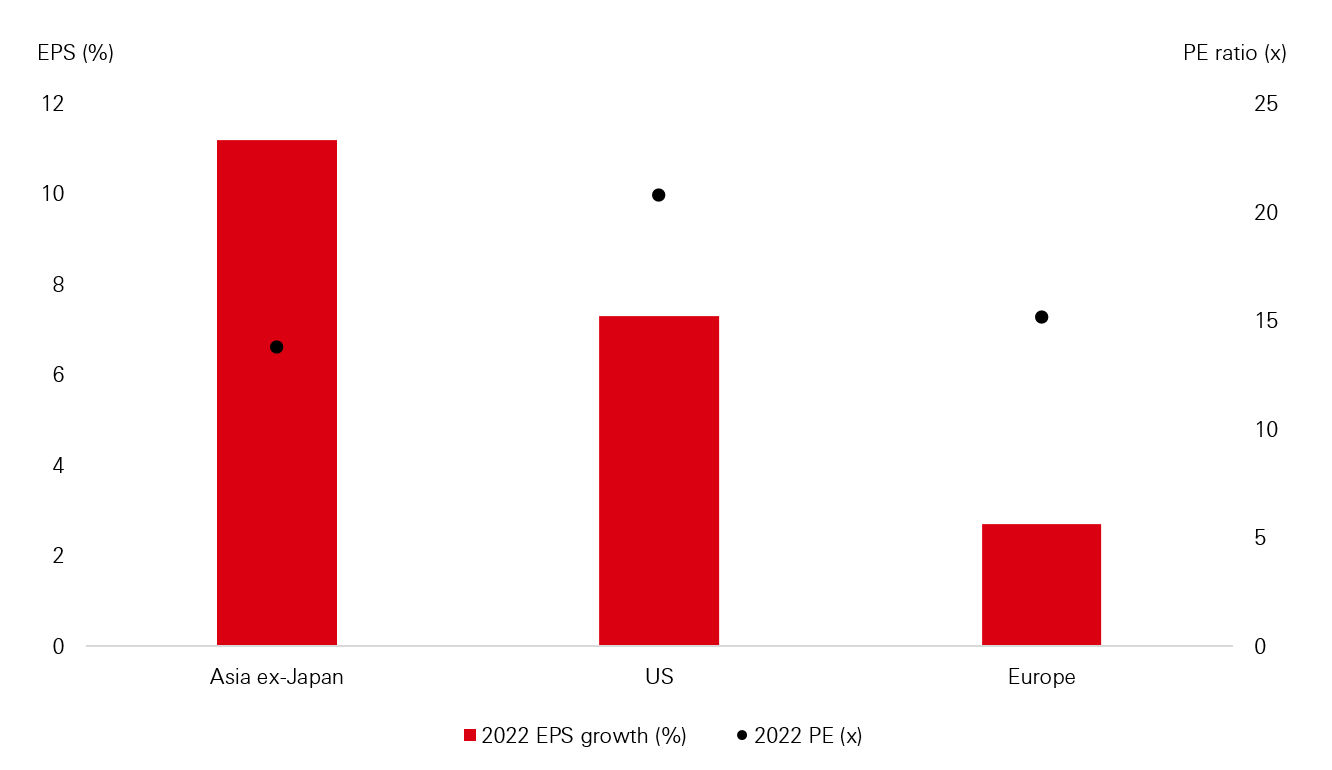

Asia expected to lead 2022 earnings growth

Asia ex-Japan equities are trading at discount to their US and European counterparts, while providing higher earnings growth

Forecasted earnings growth for Asia ex-Japan equities averages 11.2% in 2022, compared with 7.3% and 2.7% for US and European equities for the same period

At a country level, China stands out within the region as the only economy where policy is easing, which should provide a buffer against the rate tightening cycles elsewhere

Asian equities offer higher EPS growth at less demanding valuations

The performance figures displayed in the above relate to the past and past performance should not be seen as an indication of future returns.

Source: Refinitive, HSBC Asset Management, January 2022.

Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative purpose only.

Pandemic-induced digital acceleration

Tipping point - The pandemic has fast-tracked the adoption of the technology in Asia with an increasing number of consumers moving to online channels, accelerating the digital transformation of business models and the supply chain in the region. Innovation and manufacturing prowess in high tech space have also been significantly upgraded amidst the rising need for technological self-sufficiency.

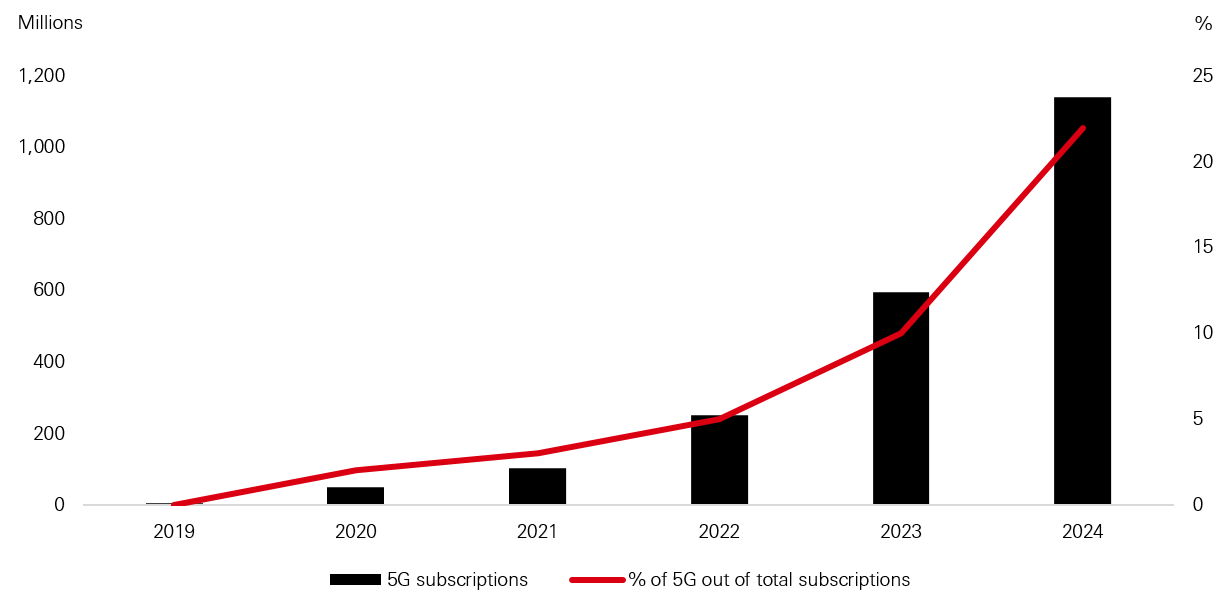

Digital adoption - In Asia, the advent of the 5G mobile technology is supported by its highly adaptable digital consumer base and government investments in “new infrastructure”, including autonomous driving, advanced healthcare, fintech and the Internet of Things (IoT). Amidst multiple driving forces, 5G subscriptions in region are expected to rise rapidly to about 1.2 billion in 2024, from less than 50 million in 2020.

Secular trend - In addition to the rise of 5G, Taiwan and Korea are home to some of the world’s largest and leading hardware and semiconductor manufacturers. These export-driven economies will likely continue to benefit from the secular trend of digitalisation – an important investment theme that could generate alpha for investors for years to come.

Asia-Pacific: 5G subscriptions (2019-2024)

Source: GlobalData’s 2020 forecast. The information provided does not constitute any investment recommendation in the above mentioned asset classes, indices or currencies. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. For illustrative purpose only.

About HSBC’s Asian equity capabilities

Note: Representative overview of the investment process, which may differ by product, client mandate or market conditions.

The Funds invest mainly in Asian equities (excluding Japan).

The Funds are subject to the risks of investing in emerging markets and smaller companies.

The Funds may invest in onshore Chinese securities through various market access schemes and China A-shares Access Products. Such investments involve additional risks, including the risks associated with China’s tax rules and practices.

Because the Funds’ base currency, investments and classes may be denominated in different currencies, investors may be affected adversely by exchange controls and exchange rate fluctuations. There is no guarantee that the currency hedging strategy applied to the relevant classes will achieve its desired result.

The Funds may invest in financial derivative instruments for investment purpose which may lead to higher volatility to its net asset value.

The Funds may pay dividends out of capital or gross of expenses. Dividend is not guaranteed and may result in capital erosion and reduction in net asset value.

The Funds’ investments may involve substantial credit, currency, volatility, liquidity, interest rate, tax and political risks. Investors may suffer substantial loss of their investments in the Funds.

Unit trusts are NOT equivalent to time deposits. Investors should not invest in the Funds solely based on the information provided in this document and should read the offering document of the Funds for details.

Beginning of dialog window. It begins with a heading called "You are leaving the HSBC AMG website.". Escape will cancel and close the window.

You are leaving the HSBC Asset Management website.

Please be aware that the external site policies will differ from our website terms and conditions and privacy policy. The next site will open in a new browser window or tab.

Beginning of dialog window. It begins with a heading called "Terms and Conditions". Escape will cancel and close the window.

Terms and conditions

This Site is intended for professional clients only.

This Site is only intended for professional clients who access it from Norway and is not intended for retail clients or other individuals, nor for U.S. Person pursuant to the U.S. Regulation S.

This Site is considered as a marketing communication.

By accessing this Site, you agree to be bound by the following terms and conditions (the “Terms”) as well as our Cookie Policy and our Privacy Notice.

Please, note that this Site is written in English only.

Categories of clients who are considered to be professionals:

Entities which are required to be authorised or regulated to operate in the financial markets. The list below shall be understood as including all authorised entities carrying out the characteristic activities of the entities mentioned: entities authorised by a Member State under a Directive, entities authorised or regulated by a Member State without reference to a Directive, and entities authorised or regulated by a third country:

Credit institutions;

Investment firms;

Other authorised or regulated financial institutions;

Insurance companies;

Collective investment schemes and management companies of such schemes;

Pension funds and management companies of such funds;

Commodity and commodity derivatives dealers;

Locals: firms which provide investment services and/or perform investment activities consisting exclusively in dealing on own account on markets in financial futures or options or other derivatives and on cash markets for the sole purpose of hedging positions on derivatives markets or which deal for the accounts of other members of those markets or make prices for them and which are guaranteed by clearing members of the same markets, where responsibility for ensuring the performance of contracts entered into by such firms is assumed by clearing members of the same markets;

Other institutional investors;

Large undertakings meeting two of the following size requirements on a company basis:

balance sheet total: EUR 20 000 000

net turnover: EUR 40 000 000

own funds: EUR 2 000 000

National and regional governments, including public bodies that manage public debt at national or regional level, Central Banks, international and supranational institutions such as the World Bank, the IMF, the ECB, the EIB and other similar international organisations.

Other institutional investors whose main activity is to invest in financial instruments, including entities dedicated to the securitisation of assets or other financing transactions.

The information presented may refer to HSBC Asset Management's global AUMs/figures and global policies. Even though local entities of HSBC Asset Management may be involved in the implementation and application of global policies, the numbers presented and the commitments listed are not necessarily a direct reflection of those of the local HSBC Asset Management entity.

Today, we and many of our customers contribute to greenhouse gas emissions. This is why HSBC Asset Management, together with other asset managers, have an important role to play in supporting the transition to a net zero economy. Step by step, we are developing strategies to reduce our own emissions and to help our customers reduce theirs. For more information visit https://www.assetmanagement.hsbc.com/about-us/net-zero

Cookies on this website

At HSBC we use cookies to help ensure that our website and services are able to function properly. These cookies are necessary and so are set automatically.

We would also like to use some cookies to:

make your visit more personal

improve our website based on how you use it

support our marketing

These cookies are optional and you can choose which types you'd like to accept. To do this, select 'Manage cookie settings'.

If you'd like to accept all optional cookies, select 'Accept all cookies'.

To learn more about how we use cookies, visit our Cookie notice.

We see Asia’s growth recovery strengthening in 2022, enabling a virtuous and sustainable economic cycle in the region

We see Asia’s growth recovery strengthening in 2022, enabling a virtuous and sustainable economic cycle in the region