China Insights

Market spotlight: Out with involution, in with innovation

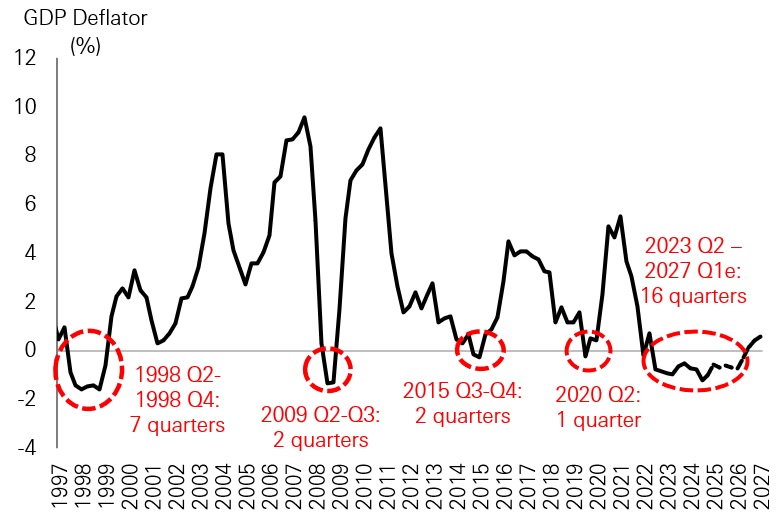

China’s economy is navigating a complex structural transition, shaped by both cyclical pressures and longer-term policy priorities. One of the most persistent challenges in recent years has been deflationary pressure, which has compressed corporate profitability and weakened incentives for investment in productivity enhancing activity. A significant contributor has been the phenomenon often described as ‘involution’, which is a destructive price competition in oversupplied industries that erodes margins and discourages innovation.

In response, policymakers introduced an ‘anti-involution’ campaign in mid-2025, targeting sectors where excessive competition had intensified disinflationary pressures. The objective extends beyond short-term stabilisation. By discouraging race-to-the-bottom pricing, authorities are attempting to reshape corporate behaviour and redirect economic incentives toward productivity, technological upgrading and higher value creation.

Figure 1: Deflationary periods in China

Click the image to enlarge

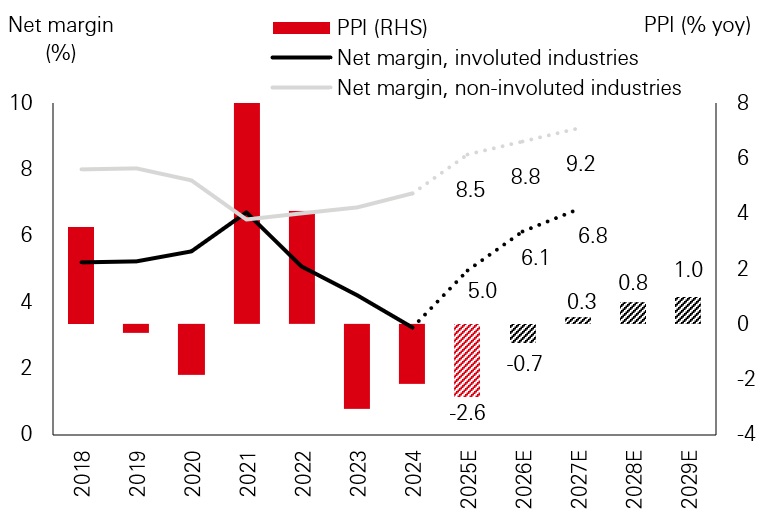

Figure 2: Forecasted impact of anti-involution on profit reflation

Click the image to enlarge

Past performance does not predict future returns. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Source: Government websites, Goldman Sachs Global Investment Research, as of January 2026.

The policy direction was reinforced at the most recent National People’s Congress (NPC), where policymakers emphasised the transition toward higher quality, innovation-led growth rather than stimulus-driven expansion. The government set a moderate growth target and reiterated its commitment to developing ‘new quality productive forces’, signalling that technological capability, industrial upgrading and domestic demand will remain the central drivers of China’s next phase of economic development. Importantly, the NPC also signalled a more explicit focus on reflation, with policymakers prioritising a return to positive price dynamics and improved corporate pricing power – a key precondition for a sustained earnings recovery.

This document provides a high-level overview of the recent economic environment. It is for marketing purposes and does not constitute investment research, investment advice nor a recommendation to any reader of this content to buy or sell investments. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination.

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

While the anti-involution initiative remains in its early stages and measurable outcomes will take time to emerge, the broader direction of policy is clear. China’s growth model is gradually shifting away from cost-driven expansion toward innovation-led development. This transition is increasingly visible across sectors such as artificial intelligence, biotechnology and advanced manufacturing i.e. the industries that feature prominently in the country’s industrial strategy.

Rebalancing toward a more resilient domestic engine

The policy agenda reflects a wider effort to rebalance the economy toward a more resilient domestic growth engine. Geopolitical tensions and trade frictions have weighed on activity in recent years, yet structural resilience remains evident. Although investment growth has slowed amid tariffs and weaker external demand, the expansion of higher value export industries – particularly technology-linked sectors – has partially offset that weakness. At the same time, supply-side reforms and industrial upgrading are helping to improve the quality rather than just the quantity of growth, reinforcing the transition toward a more sustainable economic model.

Domestic financial dynamics reinforce this shift. Following the correction in the property market, Chinese households accumulated exceptionally large savings balances, with deposits exceeding USD 20tn, a figure larger than national GDP. As deposit rates decline, a gradual reallocation of these savings into financial assets – including equities and investment funds – could provide an important source of liquidity for capital markets. Recent trends already suggest early evidence of this rotation, with increasing flows into domestic equities and Hong Kong listed markets, supported by lower deposit rates and improving sentiment toward risk assets.

Consumption patterns also illustrate the scope for rebalancing. Spending on goods is already approaching levels observed in advanced economies, yet services consumption remains underdeveloped, at roughly one-third of US levels. Policies aimed at strengthening social safety nets and reducing precautionary savings could therefore unlock a significant source of domestic demand. Policy measures announced at the NPC, including targeted support for household consumption and services sectors, reinforce this shift toward a more consumption-led growth mix.

Fostering innovation

Innovation policy sits at the centre of this transition. China’s 15th five-year plan prioritises technological capability, productivity improvement and greater economic self-reliance. Historically, the country’s development model relied heavily on scale and cost efficiency; the emerging strategy seeks to complement these strengths with technological leadership and higher value creation.

Several sectors illustrate this shift. China has established itself as a major participant in artificial intelligence, with companies such as Alibaba, Tencent and ByteDance deploying AI applications at scale.

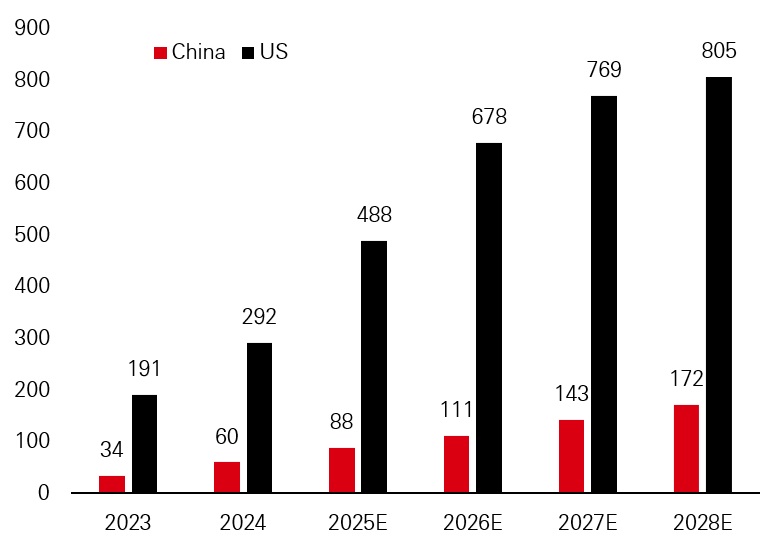

Although capital expenditure remains roughly one-fifth of US spending, Chinese firms have demonstrated notable efficiency in deploying resources and localising supply chains. Recent developments in LLMs and AI cost efficiencies have also reinforced perceptions of China's ability to compete on both performance and cost, supporting a reassessment of its innovation capabilities.

Figure 3: AI Capex for China versus major US CSP (USD bn)

Click the image to enlarge

Any forecast, projection or target where provided is indicative only and not guaranteed in any way.

Source: Bernstein analysis and estimates, January 2026.

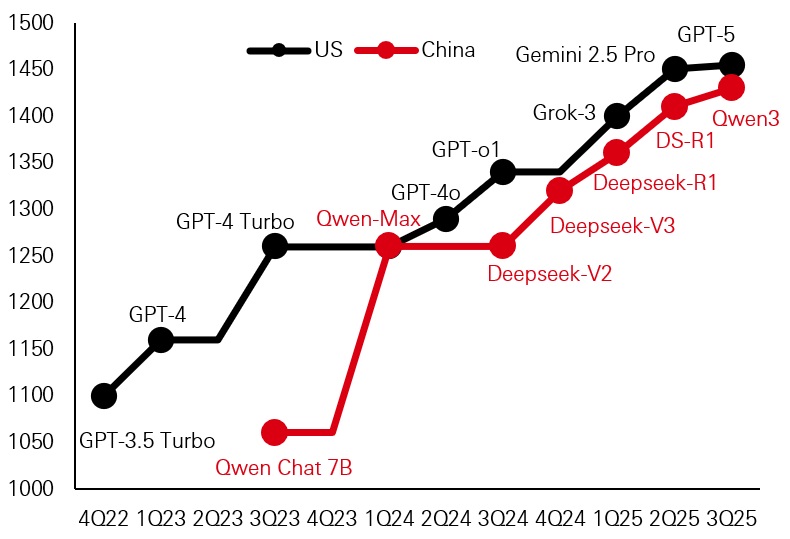

Figure 4: Chatbot arena scores for AI models

Click the image to enlarge

Any forecast, projection or target where provided is indicative only and not guaranteed in any way.

Source: Morgan Stanley Research as of December 2025.

Biotechnology represents another area of rapid progress. Chinese firms increasingly develop early stage molecules and license them to multinational pharmaceutical companies, signalling a transition from manufacturing-led growth toward intellectual property driven innovation. Meanwhile, advanced manufacturing continues to evolve toward higher precision and technology intensive production, particularly in robotics where integrated domestic supply chains allow producers to operate at materially lower cost than international competitors.

Together, these developments point to a gradual but deliberate transformation of China’s economic model. The latest NPC discussions reinforced that this transition will be supported by measured fiscal policy, targeted industrial support and a continued emphasis on technological self-reliance rather than broad-based stimulus. The policy mix therefore suggests a more calibrated approach to growth by prioritising structural upgrades, reflation and risk control over short-term stimulus cycles.

For investors, the significance lies less in short-term cyclical acceleration and more in the structural evolution of China’s growth model. As the economy moves away from deflationary competition toward productivity-driven expansion, the implications are increasingly visible across financial markets where both equities and fixed income assets are beginning to reflect the structural evolution of the economy.

China equities

Earnings repair and a gradual recovery

Against this structural backdrop, China’s equity market is moving from a valuation-led stabilisation phase toward a more earnings-driven recovery. After several years of persistent downward revisions, corporate profitability is beginning to improve, supported by easing deflationary pressures, selective fiscal measures and tighter discipline in oversupplied industries. The recovery remains uneven, yet it represents an important inflection point: equity returns are increasingly dependent on earnings quality and sustainability rather than multiple expansion alone. A gradual reflationary backdrop, supported by policy efforts to stabilise prices and improve demand conditions, is likely to be a key driver of this earnings repair cycle.

Domestic liquidity conditions have also begun to support equity market stabilisation. The gradual reallocation of substantial household savings toward higher-yielding financial assets is providing incremental support for capital markets, while policymakers have adopted a measured approach to liquidity management in order to avoid excessive volatility. This combination has contributed to a more stable upward trajectory in equity markets. Strong southbound flows into Hong Kong equities and improving participation from domestic investors further reinforce this liquidity-driven support.

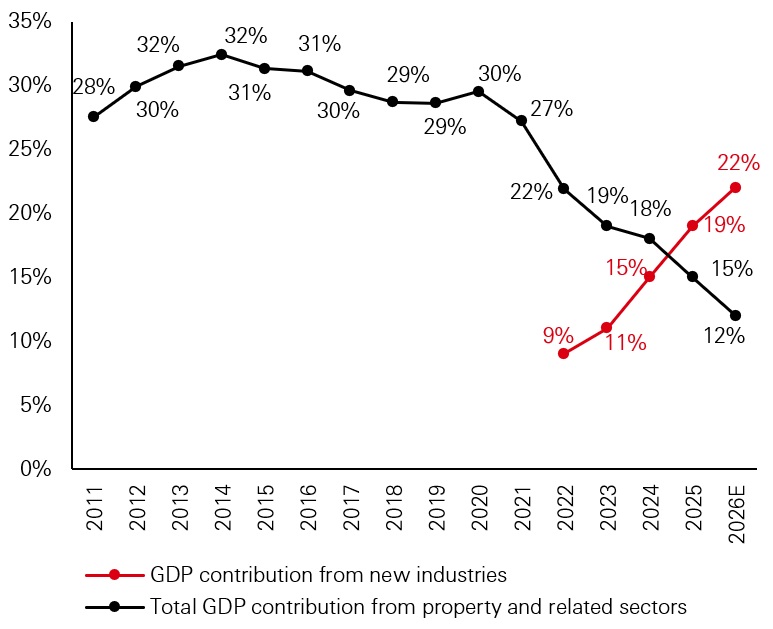

Figure 1: GDP contribution from China property sector and new industries

Click the image to enlarge

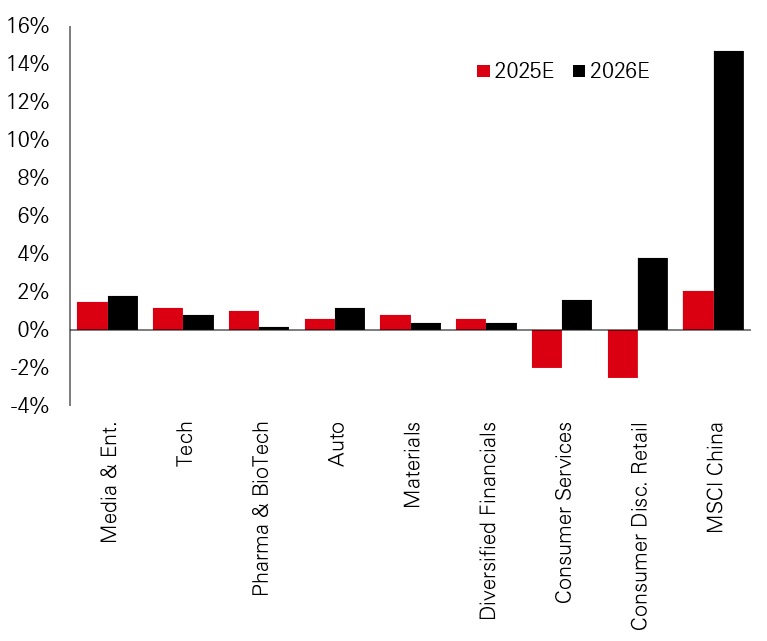

Figure 2: Consensus EPS growth estimates

Click the image to enlarge

Past performance does not predict future returns. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Source: MSCI, Bloomberg, RIMES, Factset, Morgan Stanley Research, November 2025.

At the same time, the composition of growth within the equity market is evolving. New industries – notably electric vehicles, advanced manufacturing and biotechnology – are progressively replacing real estate as the primary engine of economic expansion. This shift reflects the broader policy emphasis on innovation-driven growth and industrial upgrading.

Policy measures aimed at curbing destructive price competition have also helped stabilise corporate margins. Capacity rationalisation and regulatory intervention in sectors affected by price wars have begun to reduce margin erosion and support producer prices.

While these measures remain in the early stages of implementation, they help reduce downside risks to earnings and support a gradual rebuilding of investor confidence. Early signs of pricing discipline in upstream sectors suggest that supply-side adjustments are beginning to translate into improved profitability dynamics.

Technology and innovation-led industries remain central to the market outlook. Despite external constraints, China’s internet and technology companies continue investing heavily in artificial intelligence, automation and digital services. Monetisation pathways are gradually emerging across advertising, cloud computing, logistics optimisation and enterprise software. Although the earnings benefits of these investments are likely to be back-loaded, strong balance sheets allow companies to sustain capital expenditure without compromising financial stability.

In healthcare, rising research capability and increasing outbound licensing activity reinforce China’s growing role in global pharmaceutical development. These developments highlight the country’s increasing participation in innovation-driven industries rather than purely manufacturing-based value chains.

Consumer oriented sectors are recovering more slowly, reflecting cautious household behaviour and uneven income growth. Nevertheless, policy emphasis has shifted decisively toward supporting domestic demand, and targeted measures should gradually stabilise sentiment and moderate earnings volatility. Incremental policy support for services consumption and household income is likely to play an increasingly important role in sustaining this recovery.

Figure 3: MSCI China Forward P/E against 5-year average (x)

Click the image to enlarge

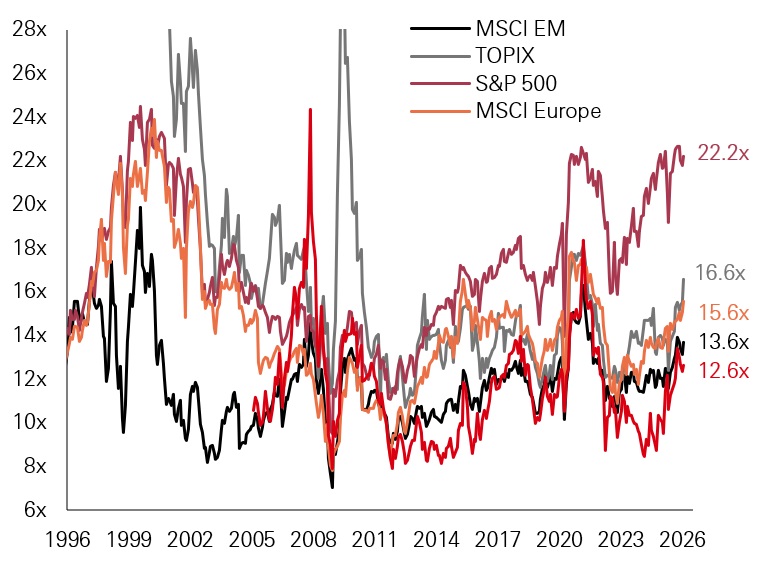

Figure 4: MSCI China Forward P/E versus global peers (x)

Click the image to enlarge

Past performance does not predict future returns. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Source: Datastream, MSCI, Morgan Stanley Research, as of January 2026.

Valuations across Chinese equities remain moderate relative to both historical averages and global peers. As a result, even incremental improvements in profitability could support medium-term returns. Combined with improving earnings visibility and policy support, this creates a more balanced risk-reward profile compared with recent years. In this environment, market performance is likely to depend less on broad macroeconomic acceleration and more on selective sectors aligned with policy priorities, margin normalisation and structural innovation.

China fixed income

Independence, diversification and the next phase

While China’s equity market reflects the country’s industrial transformation and innovation agenda, the fixed income market provides a distinct set of characteristics within global portfolios. Rather than positioning it in relative terms, its relevance lies in the specific diversification and stability properties it can offer within a multi-asset framework.

Over the past two decades, China’s bond market has undergone a remarkable transformation. What was once primarily a domestic financing channel has evolved into the second-largest bond market in the world, encompassing a broad range of sovereign, policy bank, corporate and local government issuers. The market’s development has been accompanied by gradual liberalisation, with programmes such as Bond Connect enabling foreign investors to access the domestic bond market without establishing onshore accounts.

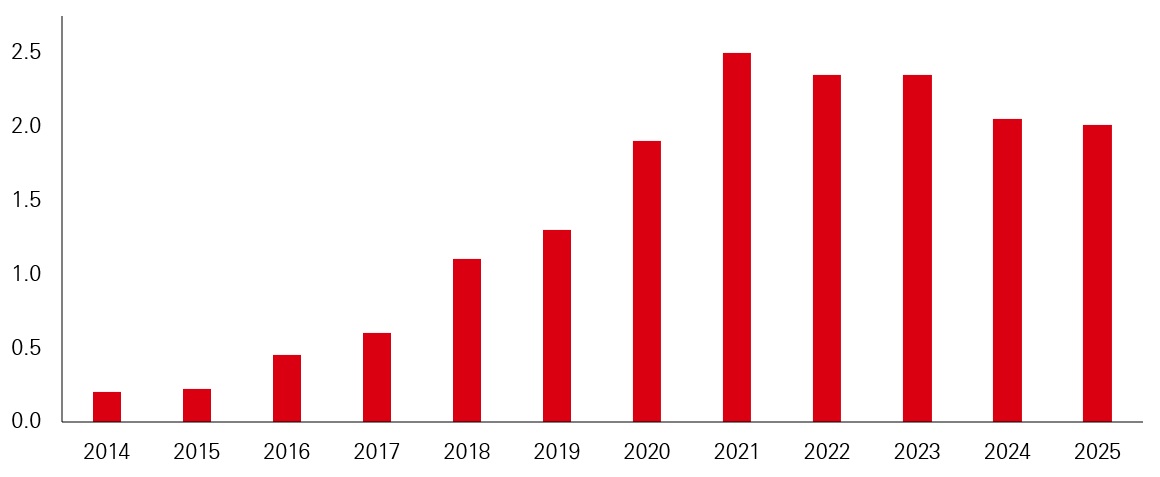

Figure 1: Foreign holdings of China government bonds (RMB trillion)

Click the image to enlarge

Past performance does not predict future returns.

Source: Bloomberg, CEIC, HSBC Asset Management January 2026.

Today, investors can allocate to Chinese fixed income through several channels, including the large onshore renminbi bond market, the offshore renminbi “dim sum” market and USD-denominated Chinese credit. Each segment offers different combinations of currency exposure, yield characteristics and credit risk, but the domestic government bond market remains the cornerstone of the asset class.

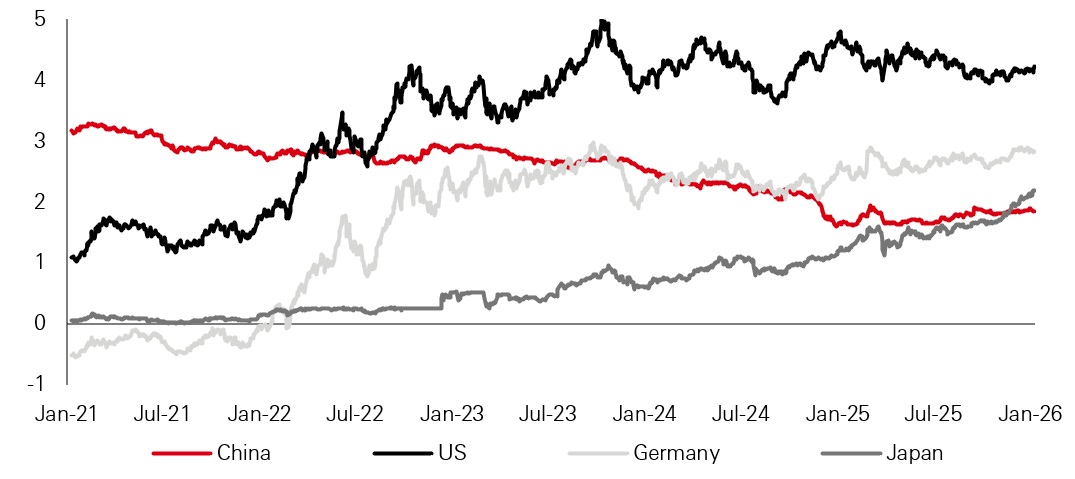

A distinctive feature of Chinese government bonds is the relative independence of their yield dynamics from global interest rate cycles. In recent years, yields in major developed markets have been driven largely by global inflation and monetary tightening cycles. Chinese government bond yields, by contrast, have been more closely linked to domestic liquidity conditions, policy objectives and growth dynamics. This reflects a policy framework that remains focused on domestic stabilisation and reflation, rather than tightly tracking global monetary cycles.

Figure 2: Yield of 10-year government bonds (per cent)

Click the image to enlarge

Past performance does not predict future returns.

Source: Bloomberg, HSBC Asset Management, data as of January 2026.

Foreign participation in the market remains modest relative to other major sovereign bond markets. As a result, international capital flows exert limited influence on yield formation. Instead, yields are primarily determined by domestic economic conditions, supply-demand dynamics and monetary policy settings.

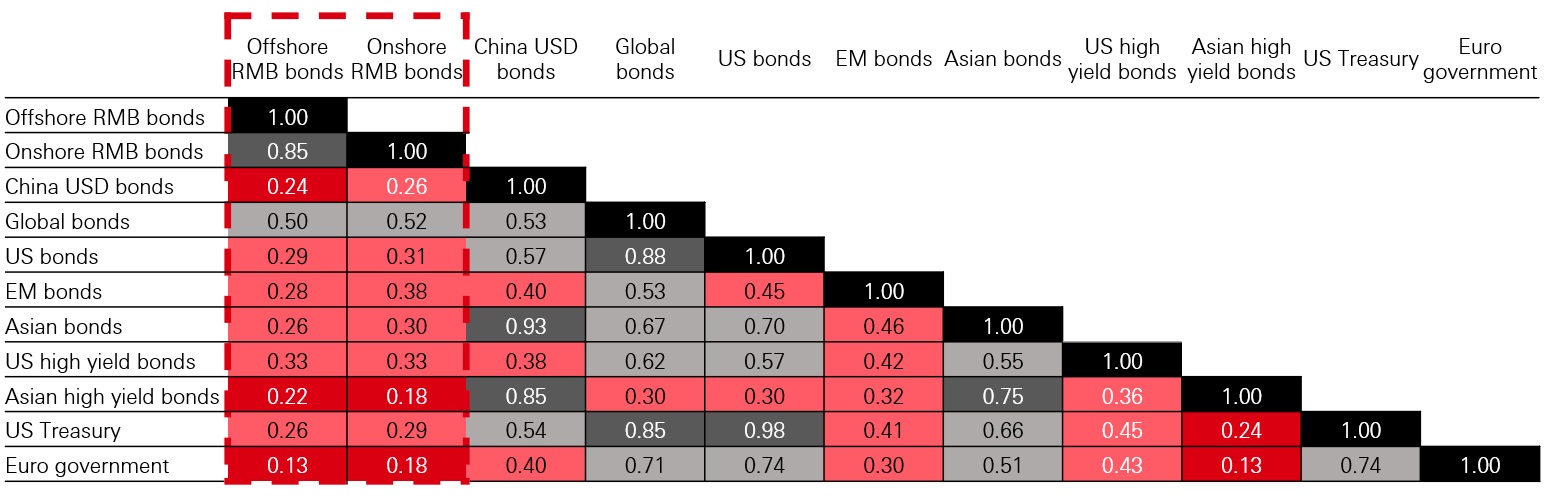

For global investors, this independence underpins the diversification case. Because Chinese bond yields respond predominantly to domestic macroeconomic factors, they have historically exhibited relatively low correlation with other major sovereign bond markets. In an environment where correlations between developed market equities and bonds have become less reliable, this feature has become increasingly valuable from a portfolio construction perspective.

Figure 3: Bond correlation in USD terms

Click the image to enlarge

Past performance does not predict future returns. Source: Bloomberg, HSBC Asset Management; Correlation calculated in USD, using weekly data for the 5-year period as of 15 December 2025. Indices used are Markit iBoxx ALBI CNH Total Return, Markit iBoxx ALBI CNY Total Return, JACI China, Bloomberg Global Aggregate Index, Bloomberg US Aggregate Index, JPMorgan GBI-EM Global Comp, JPMorgan Asia Credit Index, ICE BofA US High Yield Index, JACI Non Investment Grade Index, Bloomberg US Treasury Index, ICE BofA Euro Government Index.

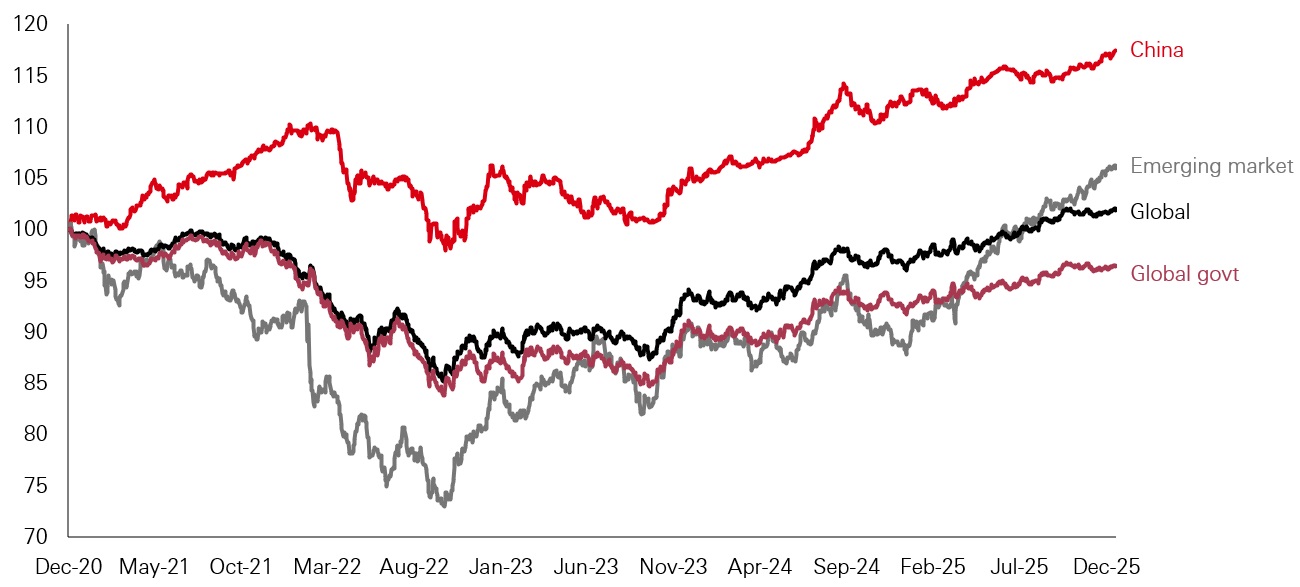

Performance data supports this perspective. Despite volatility in China’s equity market and concerns surrounding economic growth in recent years, Chinese government bonds have delivered stable returns with relatively low drawdowns compared with many global sovereign markets.

Figure 4: Total return performance (rebased to 100 on 31 December 2020)

Click the image to enlarge

Past performance does not predict future returns.

Source: Markit, JPMorgan, FTSE, Bloomberg, 16 January 2026.

Indices used: China govt bonds (unhedged USD): Markit iBoxx ALBI China Onshore Government TRI Unhedged USD; Emerging market govt bonds (unhedged USD): J.P. Morgan GBI-EM Global Diversified Composite USD; Global bonds (hedged USD): Bloomberg Global Aggregate Total Return hedged USD Index; Global government bonds (hedged USD): FTSE World Government Bond Index hedged USD.

Macro fundamentals also contribute to this resilience. China continues to maintain relatively strong external balances and growth rates that remain higher than most advanced economies. In addition, diversified energy sourcing and substantial reserves help mitigate external shocks, including periods of elevated commodity price volatility.

For portfolio construction, the implication is increasingly clear. Chinese bonds may not offer the highest yields among emerging markets, but their combination of policy anchoring, structural independence from global rate cycles and improving accessibility positions them as a valuable diversifying allocation within global fixed income portfolios.

As China’s financial markets continue their gradual integration into the global investment system, the role of renminbi fixed income within institutional portfolios is likely to expand – not as a tactical allocation, but as a strategic source of stability, diversification and income within a more complex global macro environment.

Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

Past performance does not predict future returns. Diversification does not ensure a profit or protect against loss. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

Important information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D067065; Expiry Date: 28.02.2027