Introduction

Over the past 10 years, capital raised for private market infrastructure funds has increased markedly. Investors have been attracted to infrastructure assets due to a number of favourable attributes. These can include, but are not limited to: the ability of some assets to offer inflation protection, potentially stable cash yields, defensive growth, and low correlation with other asset classes. In addition, some assets can offer benefits to portfolios in all economic conditions, particularly during periods of high inflation. This is evident for assets that benefit from long-term contracts, with revenues linked to inflation.

As the infrastructure asset class has matured, it has taken on some of the characteristics of other maturing asset classes. One of these traits is the concentration of capital being raised in large-scale funds. This has created a situation where smaller funds tend to have less competition for assets if they focus on smaller deals (smaller deals may not move the dial on returns for larger vehicles). As a result, in our view, mid-market investments present a significant opportunity, with more attractive entry valuations, historically stronger realized returns, solid growth prospects, and the potential for more varied exit options.

Given the above characteristics of mid-market assets, in our view it is not particularly surprising that these assets can have the potential to deliver outsized returns. While there are nuances to various data sources, EDHEC1 data shows that mid-markets have outperformed Core assets and the broader market over a number of time periods. We believe infrastructure investors can benefit from the opportunities to be found in the mid-market space to achieve potentially higher returns. In our previous publication, Asian Infrastructure: Filling in the Gaps, we explored this in greater detail.

Middle-market infrastructure funds – a favourable gap to target

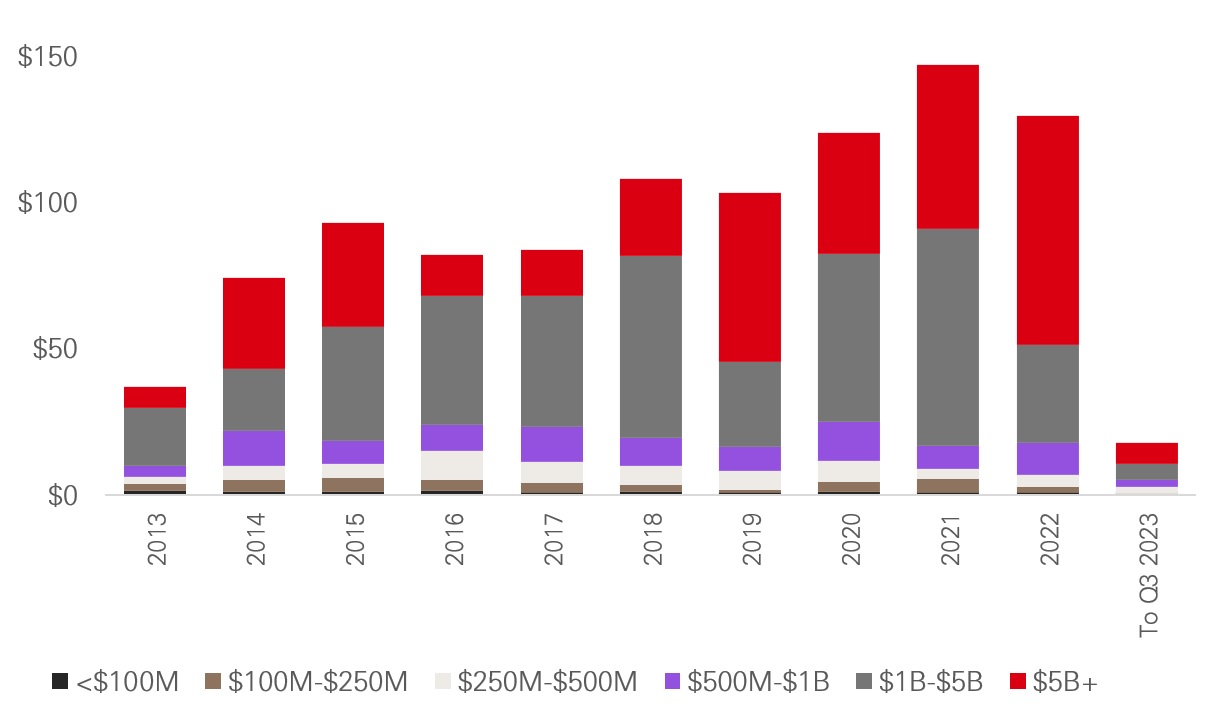

The bulk of infrastructure capital raising is focused on large-scale funds (>USD 1bn in size): an average of 76 per cent of capital raised was secured by these funds between 2013 and the end of Q3 2023.

Infrastructure capital raised by fund size (USDbn)

Source: Preqin Pro, data as of 3 April 2024

This has created an environment of competition among large-scale funds for large-scale investment opportunities. As a result of this competition, entry valuations have been driven higher over time. Arguably, the large-cap market is increasingly becoming saturated, with the main differentiator between investors simply their cost of capital, as they often compete for the same deals. While larger infrastructure funds can bring some benefits for investors, such as: a market position, perceived quality, economies of scale, and potential stability, they can also come with some constraints. These can include: the need for larger deals, competition at the top of the market increasing the price paid for assets and reducing returns. Each of these can be a limiting factor for some investors, leading them towards a mid-market alternative.

Liquidity is important too. There is a significantly higher volume of transactions in the mid-market versus the large-cap segment. Of 1,368 transactions recorded in 2023, the middle market and lower middle market accounted for 95 per cent of transaction volume, according to data from Inframation. This higher relative supply is met with less competition on the demand side, due to fewer investors focusing on the mid-market. As a result, we believe mid-market funds offer stronger prospects for alpha generation.

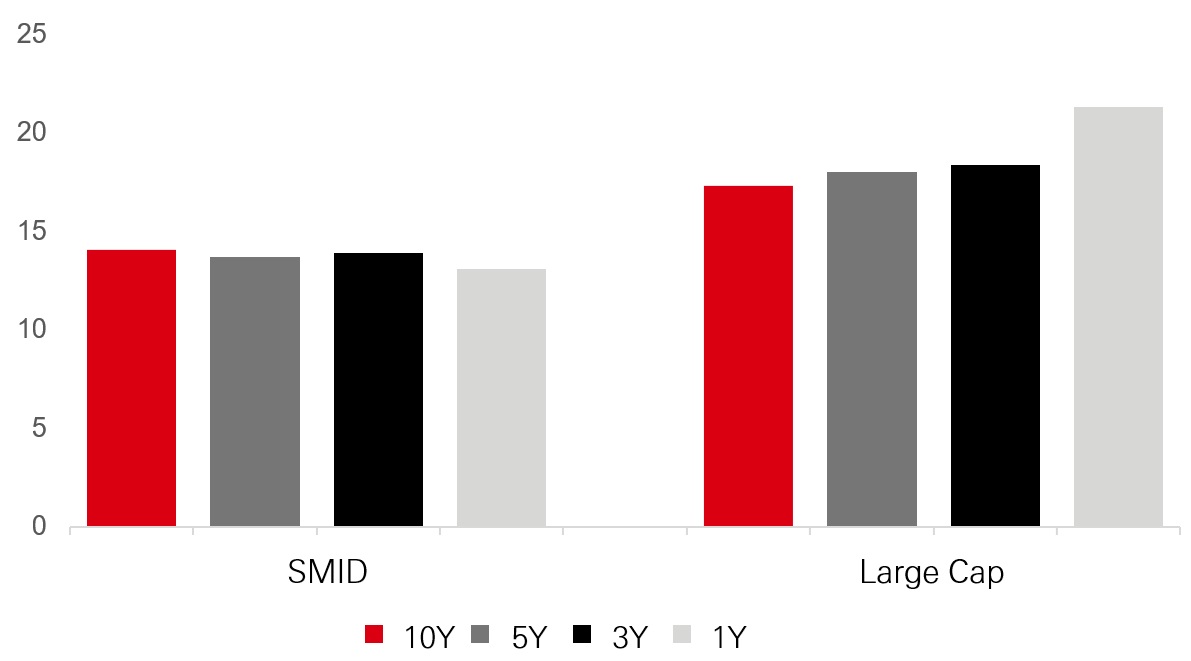

Middle-market deals can potentially offer more compelling entry multiples

In the last five to ten years, infrastructure deals in the small/mid-cap range have transacted at around a 23 per cent average discount to large and mega-cap transaction multiples, contributing to their relative outperformance.1

There are other benefits to focusing on small and mid-market opportunities. Often, small and mid-sized deals are sourced through proprietary networks instead of competitive auctions.2 This is a key point of differentiation, which has a potentially large impact upon returns. When there are auctions for assets, the price can be bid-up quite significantly in some instances. But a wide network of contacts within the infrastructure industry can mean that assets are marketed ‘under the radar’ and without the competition associated with an auction. In these instances, a solid network is vitally important.

Average EV/EBITDA Multiple for Infrastructure Transactions

Source: Hamilton Lane Analysis, DWS proprietary database of European unlisted infrastructure deals, including publicly available transaction information from Infrastructure Journal, InfraNews, Pitchbook, Bloomberg, Preqin, Inframation as of June 2024

Mechanisms

We believe reduced competition for small and mid-cap assets, asset class characteristics and difficulty with sourcing deals can explain some of the differences in returns between fund sizes. At the same time, risk is, obviously, also a key factor.

Larger funds are typically constrained by mandate and resource towards a minimum deal size that precludes assessing and investing in mid-sized firms. They also typically compete at that size alongside non-financial, or “strategic” investors, such as large utility, energy or infrastructure companies, who are also searching for scale. With larger funds competing for fewer larger deals, mid-sized firms are the preserve of smaller funds, which can often be acquired on more favorable terms.

Mid-market deals can also offer access to market segment that is relatively inaccessible to large-cap funds, including platform buildouts, roll-up, or aggregation strategies that cannot be executed on a scale large enough for large-cap infrastructure funds.

Smaller funds can take advantage of proprietary sourcing capabilities and platform scale-up opportunities (both organic and inorganic). Small and mid-market assets can also offer more routes to valuation uplift. For example, if a manager can acquire a mid-market asset and successfully grow it into a large-cap asset by the time of sale, it is likely to experience a valuation uplift, as it could become at acquisition target for larger funds or strategic investors.

Performance in perspective

With a prudent approach to manager selection and disciplined execution, mid-market funds can potentially outperform large-cap funds. One way in which to see the opportunity is to look at the assets that would form the investments of small or mid-market funds, compared to assets that might sit within large-scale funds. While a generalisation, we believe larger assets are likely to be bigger, lower risk and potentially generating stable cash flows. This might put many assets within the Core ‘bucket’.

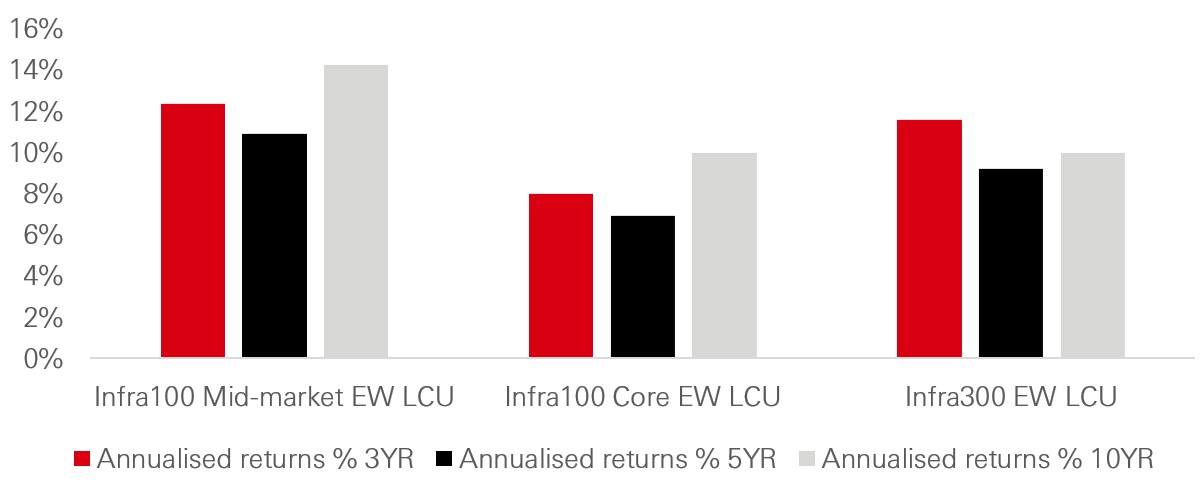

Infrastructure returns

Source: EDHEC, data as of July 2024

We can see that mid-market assets have generated significant returns over the long-term, particularly when compared to Core assets and the broader index of assets. This backs-up the assumption that smaller assets can outperform their larger counterparts. In our view, while the performance highlighted is at the asset level, it is sensible to assume that the assets which would sit in mid-market or large-scale funds would comprise similar assets to those in the respective indices. This gives us some comfort in our preference towards mid-market assets.

Bigger is not always better

Size can often have a more significant effect in private markets than public markets. We believe this is particularly true in the infrastructure asset class. And within that, in our view, the infrastructure middle market offers a particularly interesting opportunity. While returns from mid-market assets are greater than Core assets over the long-term, we believe they also offer additional diversification benefits, through providing assess to parts of the market off-limits to those which invest only in larger funds.

Within the infrastructure middle market, we believe the opportunity in energy transition infrastructure stands out. If net zero targets are to be delivered, energy transition investment will need to increase significantly from present levels. This will not be delivered by governments alone, so private capital markets have an important role to play. No single asset will deliver on the net zero target, and a broad composition of large and smaller-scale projects will have to be utilized. This is a key driver of our belief in the mid-market and our area of focus.

Past performance is not indicative of future performance.

1. École des Hautes Etudes Commerciales du Nord

2 Hamilton Lane, The Infrastructure Middle Market is Ripe with Opportunity

3. Schroders, The attractions of the small-mid private equity segment as of 6 June 2024

Any views expressed were held at the time of preparation and a re subject to change without notice.

Risk Considerations: There is no assurance that a portfolio will achieve its investment objective or will work under all market conditions. The value of investments may go down as well as up and you may not get back the amount originally invested. Portfolios may be subject to certain additional risks, which should be considered carefully along with their investment objectives and fees.

Illiquidity: An investment in alternatives is a long-term illiquid investment. By their nature, alternatives’ investments will not generally be exchange traded. These investments will be illiquid.

Long term horizon: Investors should expect to be locked-in for the full term of the investment.

Economic conditions: The economic cycle and prevailing interest rates will impact the attractiveness of the underlying investments. Economic activity and sentiment also impacts the performance of underlying companies and will have a direct bearing on the ability of companies to keep up with interest and principal repayments.

Valuation: These investments may have no or a limited liquid market, and other investments including those in respect of loans and securities of private companies, may be based on estimates which cannot be marked to market until sale. The valuation of the underlying investments is therefore inherently opaque.

Market risk: There is no guarantee in respect of the repayment of principal or the value of investments, and the income derived therefrom may fall as well as rise. Investors therefore may not recoup the original amount invested in the Partnership. In particular, the value of investments may be affected by political and economic news, government policy, changes in technology and business practices, changes in demographics, cultures and populations, natural or human-caused disasters, pandemics, weather and climate patterns, scientific or investigative discoveries, costs and availability of energy, commodities and natural resources. The effects of market risk can be immediate or gradual, short-term or long-term, narrow or broad.

Political and economic risks: General economic conditions may affect the activities. Changes in economic conditions, including, for example, inflation, unemployment, competition, technological developments, political events and other factors, none of which will be within the control of the General Partner or the service providers, can substantially and adversely affect the business and prospect investors. Due to the geographic scope of its activities, the strategy may be vulnerable to country or regional-specific political, macroeconomic and financial environments or circumstances.

Sustainability risk: Sustainability risk means an environmental, social or governance event or condition that, if it occurs, could cause an actual or a potential material negative impact on the value of the investment.

Alternatives: There are additional risks associated with specific alternative investments within the portfolios; these investments may be less readily realisable than others and it may therefore be difficult to sell in a timely manner at a reasonable price or to obtain reliable information about their value; there may also be greater potential for significant price movements.

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group). The above communication is distributed by the following entities:

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only, and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- in Bermuda by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- in Chile: Operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- in Colombia: HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- in France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- in Germany by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This video/content has not be reviewed by the Securities and Futures Commission;

- in India by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- in Italy and Spain by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- in Malta by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- in Mexico by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- in the United Arab Emirates, Qatar, Bahrain & Kuwait by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Securities and Commodities Authority in the UAE under SCA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- in Peru: HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- in Singapore by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments;

- in Taiwan by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- in Turkiye by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- in the UK by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- and in the US by HSBC Global Asset Management (USA) Inc. which is an investment adviser registered with the US Securities and Exchange Commission.

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2025. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management Limited.

Content ID: D022299_v5.0 ; Expiry Date: 30.09.2026